Patch Management Market Set to Double, Forecast to Reach USD 1.45 Billion by 2029

Market Size

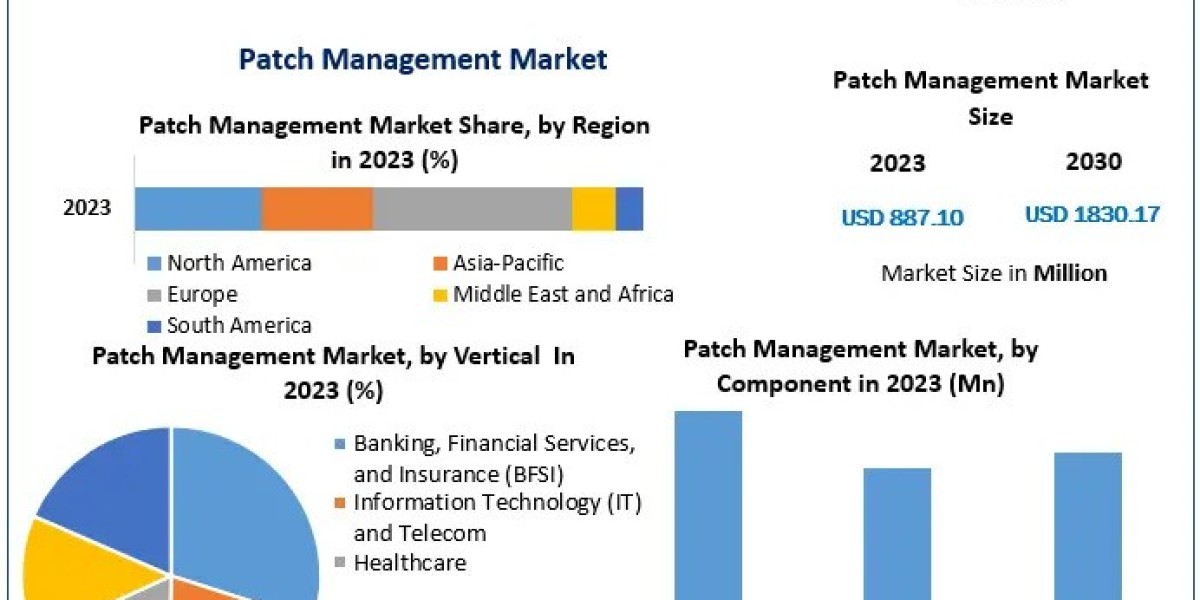

The global patch management market was valued at approximately USD 724 million in 2023 and is projected to reach USD 1.45 billion by 2030, exhibiting a robust CAGR of 10.4%.

Overview

Patch management involves identifying, acquiring, installing, and verifying patches for software systems—critical for mitigating security vulnerabilities. These solutions span software platforms and managed services, deployed across on-premises and cloud environments. The ongoing increase in cyber threats, widespread cloud adoption, and demand for automated security operations are propelling the patch management market forward.

To Know More About This Report Request A Free Sample Copy https://www.maximizemarketresearch.com/request-sample/33698/

Market Estimation & Definition

This market comprises software tools and services designed to automate tracking and installation of security patches and updates across digital infrastructures. Covering both self-managed (on-premises) and cloud-based deployments, the patch management ecosystem ensures compliance and protection for enterprises by reducing exposure to exploits and enhancing vulnerability response.

In 2023, market revenue stood at USD 723.6 million, with projections doubling by 2030 to reach USD 1.45 billion, growing at a 10.4% CAGR.

Market Growth Drivers & Opportunities

- Rising Cyber Threats & Compliance Needs: Global increases in vulnerabilities, malware, and patch-related exploits are prompting stricter industry standards and regulatory pressure.

- Cloud Migration: The shift toward cloud and remote work models is boosting demand for scalable, centralized patch management solutions.

- Automation with AI/ML: Adoption of AI-driven patch prioritization and automated deployment is simplifying vulnerability mitigation.

- SME & Healthcare Expansion: Small and medium-sized enterprises and healthcare providers are rapidly adopting patch services to secure endpoint-heavy environments.

- Integration into Broader IT Ecosystems: Seamless integration with ITSM, DevSecOps pipelines, and security platforms via API and platform synergy presents new market entry points.

Market Scope

- Base Year: 2023

- Forecast Period: 2024–2030

- Market Value (2023): USD 723.6 million

- Projected Market Value (2030): USD 1.45 billion

- CAGR: 10.4%

Segmentation Analysis

By Solution:

- Software (largest segment by revenue in 2023)

- Services (fastest growing segment, managed and consulting offerings)

By Deployment:

- Cloud-Based (dominant, high scalability and remote management)

- On-Premises (growing due to control and regulatory needs)

By Enterprise Size:

- Large Enterprises (significant revenue share)

- SMEs (fastest CAGR, driven by distributed workforces)

By Vertical:

- IT & Telecom (leading segment)

- BFSI (high demand due to security and compliance)

- Healthcare (rapid growth)

- Retail & eCommerce

- Manufacturing

- Energy & Utilities

- Government

- Others (Media, Logistics, Transportation, Defense)

Major Manufacturers

- Microsoft

- Broadcom

- IBM

- VMware

- Qualys

- SolarWinds

- Automox

- Kaseya

- Freshworks

- NinjaOne

- SysAid

- Heimdal

- Avast

Regional Analysis

United States (North America):

Leading regional market with ~37–40% market share, driven by advanced IT infrastructure, high regulatory standards, and early cloud adoption.

Germany (Europe):

Part of Europe’s strong patch market (~25–30% share), with growth fueled by GDPR compliance, cybersecurity awareness, and industrial automation.

Asia-Pacific:

Fastest-growing region (~13% CAGR), led by China and India. Growth stems from rapid digitalization, expansion of telecom and IT ecosystems, and increasing cybersecurity regulations.

COVID-19 Impact Analysis

The pandemic disrupted supply chains and delayed patch management tool deployments initially. However, it also accelerated digital transformation and remote work adoption—heightening security concerns and driving investments in automated patch solutions. The market rebounded quickly and sustained strong growth.

Commutator Analysis

Patch management systems don't feature mechanical commutators but rely on intelligent automation workflows:

- Vulnerability Prioritization: AI-enriched capabilities rank patches by risk, enabling efficient remediation.

- Automation & Integration: From vulnerability scanning to deployment, auto-driven patching reduces human error.

- Deployment Models: Cloud models offer quick rollouts; on-premises systems provide tight control.

- Performance & Control Trade-offs: Organizations choose systems based on infrastructure complexity, workforce distribution, and policy compliance.

Key Questions Answered

- How big is the patch management market now and in 2030?

USD 723.6 million in 2023; projected at USD 1.45 billion by 2030. - What is the CAGR?

10.4% from 2023 to 2030. - Which solution leads?

Software leads revenue; services grow fastest. - What deployment model is dominant?

Cloud-based solutions dominate; on-premises retain strong segments. - Which enterprise size segment grows fastest?

SMEs exhibit the highest growth due to scalable, remote-friendly solutions. - Which industry verticals are driving adoption?

IT & Telecom, BFSI, and Healthcare lead adoption. - Which regions lead and grow fastest?

North America leads; Asia-Pacific grows fastest. - How did COVID-19 impact this market?

Rebound fueled by remote work and infrastructure modernization. - What technology trends are shaping the market?

AI/ML integration, DevSecOps workflows, ITSM convergence, and vulnerability-first patching.

About Maximize Market Research

Maximize Market Research Pvt. Ltd., based in Pune, India, is a global market intelligence provider. Specializing in tech, industrial, and healthcare sectors, the firm delivers strategic research and insights to support enterprise decision-making and growth in evolving markets worldwide.

Conclusion

With cybersecurity threats intensifying and digital infrastructure expanding, the global patch management market is steadily approaching USD 1.45 billion by 2030. Automation, cloud integration, and intelligent patch prioritization are key enablers. As organizations—including large enterprises, SMEs, and highly regulated industries—uphold digital resilience, the adoption of patch management solutions will be indispensable. Stakeholders must focus on scalable deployment models and integrated workflows to capitalize on this critical cybersecurity frontier.